BBVA: Financiación simple y accesible para hispanos en EE. UU.

Being denied a loan can be disappointing and challenging, especially when you were planning to use those funds for something important. Unfortunately, there are a number of factors that can lead to a loan denial, such as a negative credit history, insufficient income, or lack of collateral. However, don’t despair. There are a few things you can do if your loan is declined.

In this article, we will explore some strategies that can help you overcome this situation and find alternatives to achieve your financial goals.

Receiving a refusal when applying for a loan can be extremely frustrating and confusing. We’ve all been through times when we need extra money, and when that happens, a loan may be the most viable solution. However, several factors can lead to a loan denial.

It is important to remember that each financial institution has its own policies and loan approval criteria, so it may be useful to look for other options. By having a clearer understanding of why your loan was declined, you can make the necessary adjustments and try again successfully in the future.

Understanding the reasons for your loan being declined can be quite frustrating and often difficult to understand. However, it is essential to understand that banks and financial institutions have specific criteria and policies for approving or denying a loan.

After receiving news that your loan application has been declined, it’s normal to feel discouraged and worried about your finances. However, it is important to remember that not all is lost. There are steps you can take to resolve this situation and find viable alternatives for your financial needs.

It’s important to remember that there is no magic solution to solve all financial problems. However, by following these steps and looking for alternative solutions, it is possible to overcome loan denial and find ways to manage your finances more efficiently.

Obtaining credit can be a difficult task for many people, especially for those who do not have a solid financial history or have a negative credit rating. However, there are alternative options that can help overcome this situation and make it possible to obtain credit even in times of difficulty.

One of the options is to look for loans on digital platforms, known as fintechs. These companies offer credit more easily and quickly, often without the need for proof of income or guarantor. Furthermore, interest rates are usually lower than those charged by traditional banks.

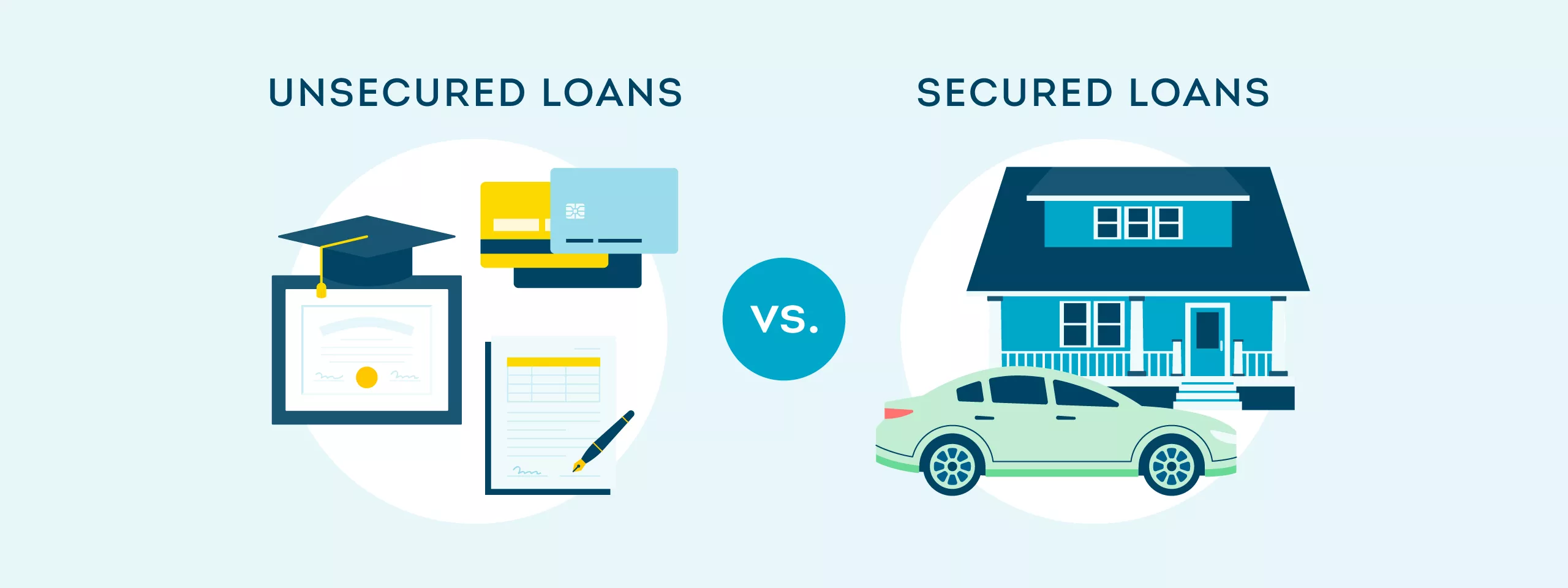

Another alternative is to use a secured loan, such as a payroll loan. In this type of credit, an asset is offered as collateral, such as a property or a vehicle, which reduces the risk for the financial institution. Because of this, interest rates are also lower and the amount available for loan may be higher.

If it is not possible to obtain credit through the previous options, an alternative option is to resort to loans between individuals, known as peer-to-peer lending. In this model, platforms connect people who have money to invest with people who need loans. Interest rates can vary and it is important to do your research before choosing this option.

Many people avoid reviewing their financial situation because they are afraid of what they will find. However, it is extremely important to face this task and do an in-depth analysis of your finances. Reviewing your financial situation regularly can bring several benefits, such as enabling better organization, preventing future problems and setting realistic goals for the future.

By reviewing your financial situation, you will have a clear picture of where you are spending your money. This will allow you to identify areas of waste and take steps to reduce unnecessary spending. Additionally, you will be able to organize your expenses and prioritize your spending more efficiently.

Another advantage of reviewing your financial situation is preventing future problems. By analyzing your expenses, you can identify potential debts or expenses that are piling up. This way, you can take preventative measures, such as cutting expenses or looking for alternative income, before these problems become too big and difficult to solve.

Finally, reviewing your financial situation will allow you to set realistic goals for the future. By evaluating your current income and expenses, you can set achievable financial goals, such as saving for a trip, investing in your education, or paying off debt. With clear goals in mind, you’ll be more motivated to save and stay on track for financial stability.

Dealing with a loan denial can be a frustrating and challenging situation. It can be difficult to accept the fact that your application was rejected, especially if you were counting on this money for an important project or emergency. However, it is essential to maintain a positive outlook and not let the denial affect your state of mind or your future attempts to obtain credit.

First of all, it is important to understand the reasons for loan refusal. Financial institutions often have strict criteria and specific policies when evaluating customers’ ability to repay their debts. This could include poor credit history, lack of stable income, or even issues with documentation. By understanding the reasons why you were denied a loan, you will be in a better position to work through these issues and improve your financial situation.

Second, try not to take loan denial personally. Remember that credit granting criteria are often determined by external factors, such as bank policies or government regulations. Refusal is not an indication of your own financial capacity. Instead, view it as an opportunity to learn and strengthen your credit profile. Look for ways to improve your credit score, such as paying your debts on time, reducing your monthly expenses, and avoiding unnecessary new debt.

Finally, don’t be discouraged and don’t give up on getting a loan. There are several alternatives available, such as credit unions, fintechs and online loans. Do detailed research and find financial institutions that can meet your needs and criteria. Also consider asking family or friends for help, or seeking other sources of financing, such as crowdfunding. Remember to maintain a positive attitude and persevere in your search for credit.

Getting a loan can be an important step towards achieving your financial goals. Whether it’s paying off debts, investing in a business or making a dream come true, having access to credit can make all the difference. However, you need to follow some steps before applying for a loan.

By reading this complete guide, with tips and step-by-step instructions, be prepared to get your loan in a safe and conscious way. Evaluate your options, know your financial profile and be aware of the responsibilities involved. With planning and organization, you will be closer to achieving your financial goals.

{kind=link}